2 October 2025

Amr Hussein Elalfy

Background

- On 31 July 2025, Raya Customer Experience [RACC] disclosed that its parent company Raya Holding for Financial Investments [RAYA] formally notified the Financial Regulatory Authority (FRA) of its intention to launch a mandatory tender offer (MTO) to acquire up to 90% of RACC’s capital at an initial price range between EGP6.87 and EGP7.5 per share.

What happened?

- Almost two months later on 28 September 2025, RACC received the FRA approval to publish the MTO, with the following details:

- RAYA is offering to acquire up to 43,952,433 shares of RACC, equivalent to 22.1% of RACC’s issued shares net of 5,916,785 treasury shares that are more than one year old (i.e. 199,206,202 shares, which is 205,122,987 issued shares less the 5,916,785 treasury shares).

- The final MTO price is set at EGP7.50 per share, the maximum of the initial price range.

- The MTO runs for 20 working days from 28 September through 26 October 2025.

- Execution of the MTO will be within 5 working days after the end of the MTO (i.e. by maximum 2 November, according to our calculation).

- RAYA’s goal is to raise its ownership in RACC up to 90% from its current 59.9%.

- RAYA does not have any intention to merge RACC into any other entity for the time being.

What is an MTO and why do it?

- According to the Executive Regulations of the Capital Market Law No. 95/1992 (Chapter VI, Article No. 353), when an investor wants to acquire a certain stake in a target company either independently or through related entities, it has to submit what is known as a mandatory tender offer or MTO to acquire up to 100% of the target company. Such MTO is triggered when the targeted stake is either 33.3%, 50%, 67.7%, or 75% of the target company or more.

- MTOs are one of the tools that the FRA uses to protect the interest of minority shareholders in a company listed on the Egyptian Exchange (EGX). Through the MTO, minority shareholders are given the opportunity to accept the offer being made for the target company’s shares at the announced offer price.

- However, if the acquirer intends to keep the target company listed on the EGX, the MTO will be for the maximum number of shares that the acquirer can buy while keeping the required minimum number of shares for the target company to remain listed on the EGX.

- According to the EGX Listing and Delisting Rules (Section II, Article No. 7), to remain listed on the EGX, a company has to meet the minimum allowed percentage to remain listed on the EGX, its free float shares must not be less than (a) 10% of its listed shares or (b) 0.0125% of the EGX’s free-float market cap, provided that it does not fall below a minimum of 5% of its listed shares.

What choices do I have?

- If you are a shareholder in RACC, you have the choice to do one of two things:

- Accept the MTO and register your shares through your broker on the OPR system during the aforementioned MTO period to receive the MTO price per share (i.e. EGP7.50 per share).

But when will you consider accepting the MTO?

If MTO price is higher than the market price and its fair value.

- Reject the MTO by simply doing nothing. In other words, do not submit your shares in the MTO, hence you will continue to hold on to your shares.

But when will you reject the MTO?

If MTO price is lower than the market price and its fair value.

- If you are not a shareholder in RACC, you need to assess the situation to make an investment decision, as follows:

- Consider the MTO price versus the market price. If the MTO price is higher than (i.e. at a premium to) the market price (not the case today), then there might be a good chance to make a profit within a month by buying RACC in the market at a price that is lower than the MTO price. However, you need to consider:

- The time value of money (since your sale proceeds will only show up on your account at the start of November).

- The opportunity cost of locking up some liquidity in RACC, thus forgoing other investment opportunities in the market that may generate a relatively higher return over the same time period.

- Consider the MTO price versus the stock’s fair value. If the MTO price is lower than (i.e. at a discount to) the stock’s fair value, then the MTO will likely confirm the acquirer’s (RAYA in this case) point of view that the stock is worth more than the MTO price. Thus, you might decide to jump on the bandwagon of RACC by investing at a price that you believe is below its fair value with the hope that the stock will move higher over time.

- Consider the MTO price versus the market price. If the MTO price is higher than (i.e. at a premium to) the market price (not the case today), then there might be a good chance to make a profit within a month by buying RACC in the market at a price that is lower than the MTO price. However, you need to consider:

What does this all mean for RACC?

- At EGP7.5 per share, the MTO values RACC at roughly EGP1.44 billion.

- RACC will remain listed on the EGX but potentially with a lower free float (at least 10%).

- RAYA reiterated that there is no immediate plan to take RACC private or to merge it with any other entity, so it will be business as usual, except for RAYA’s intention to:

- Expand RACC’s activities through partnerships with leading companies.

- Streamline RACC”s operations to capture synergies.

Valuation

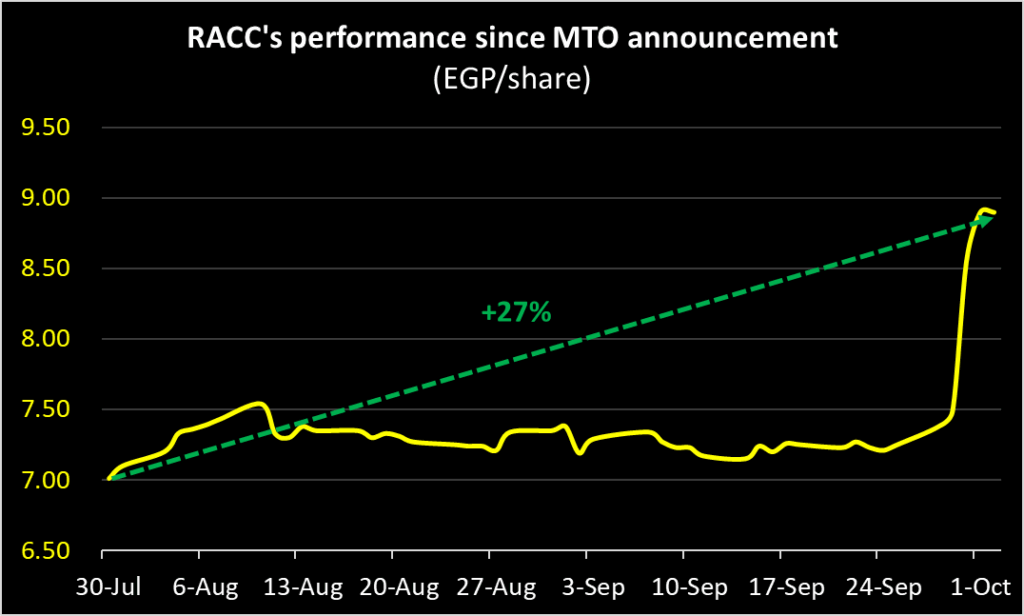

- On 30 July 2025, RACC was trading at EGP7.01 per share, 7% below the higher end of the MTO price range announced back then.

- From 31 July through 28 September 2025, RACC traded at a 3% discount to the higher end of the MTO price range.

- After the final MTO price (i.e. EGP7.50 per share) was announced, RACC rallied by as much as 31% versus the MTO price to an intraday high of EGP9.80 per share on 1 October.

- By the end of 2 October, RACC closed at EGP8.90 per share or 19% above the MTO price.

- To put things into perspective:

- At the time of RACC’s IPO back in 2017, the company was valued at EGP1.65 billion or equivalent to USD91 million at then-prevailing FX rates.

- Today, the MTO implies a valuation of EGP1.44 billion or just USD30 million at an FX rate of EGP48/USD, which is around a third of its IPO valuation.

- In terms of its earnings multiples, the MTO price values RACC at around 6x last 12-month (LTM) earnings), quite below both its historical and peers’ levels.

Recommended action

- We see the MTO as a meaningful development that could help RACC stock approach its fair value as per our estimates.

- Since the MTO was published, RACC’s stock price rose by more than 20% in four trading days, signaling a positive market reaction. This might suggest two things:

- Investors are betting that the MTO price could be raised over the coming few days, especially if the independent financial advisor’s (IFA) valuation came out to be higher than the MTO price.

- Investors believe RAYA’s move to consolidate its stake in RACC further aligns its interest with theirs, opening the door for more value creation down the road and affirming its confidence in RACC’s long-term prospects.

By: Amr Hussein Elalfy, CFA & Mohamed Hosny

The Good

- VALU is a pioneer in the BNPL space, outgrowing the consumer finance industry

- VALU’s diversified approach resulted in a massive market share growth in a shrinking auto market

- VALU’s growth was reflected in its profitability ratios, mainly ROE

- AI-driven risk management to address surging growth, while maintaining a solid risk profile

- A well-recognized fintech player with a strong brand equity benefiting from the first-mover advantage

- A beneficiary of the networking effect, driven by its transaction volume leadership

- Access to finance through banks and non-banking financial institutions

- A proven track record by an innovative young management team disrupting the industry

The Bad

- A market with low barriers to entry with rising competition from new entrants

- No cash dividend plans in the foreseeable future

- Potentially a limited free float percentage

- The risk of any of the current pre-transaction shareholders selling off

- If interest rates reverse direction higher or rate cuts come in slower than expected

- If VALU approaches the maximum allowed leverage threshold

- If the market dries up with demand for securitization faltering

The Catalysts

- Regional expansion to drive growth

- Declining interest rates in Egypt to reduce funding cost

- Declining inflation rates in Egypt to drive demand

- Utilizing current leverage buffer to support further growth

- Any potential acquisition of VALU could drive growth further

Key Metrics

- IFA valuation: EGP 15.59 billion (EGP 7.4/share)

- 2024 / Q1-2025 Book value: EGP 1.64 billion (EGP 0.777/share) / EGP 1.76 billion (EGP 0.836/share)

- 2024 / 2025e P/E: 36.9x / 23.9x

- 2024 / 2025e P/BV: 9.5x / 6.8x

- 2024 / 2025e tangible P/BV: 13.4x / 8.5x

- 2024 / 2025e ROAE: 30% / 33%

- 2024 / 2025e ROATE: 45% / 43%

The Story

VALU [VALU] (officially named U Consumer Finance) is a leading financial technology (fintech) platform, offering a suite of financial services to individuals and businesses. Since its launch in 2017, VALU has continued to provide a wide range of consumer finance products.

As a pioneer of BNPL (Buy Now, Pay Later) solutions, VALU is the No. 1 player in that market segment, providing customizable financing plans for up to 60 months across more than 6,000 points of sale and over 1,500 online stores, covering a diverse array of categories.

In addition to its lending and payment services, VALU also offers investment products, an instant cash redemption program, savings solutions, and a financing solution to facilitate the purchase of big-ticket items up to EGP 15 million in the luxury space.

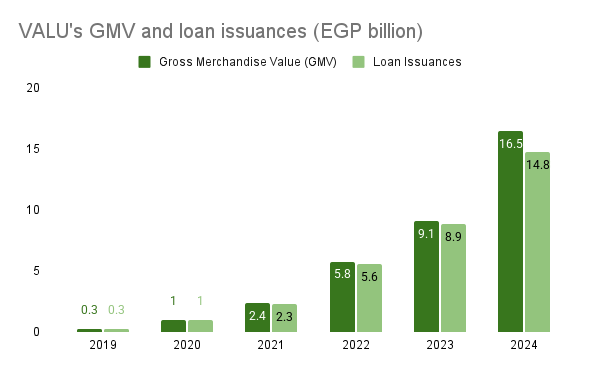

In 2024, VALU issued a total of EGP 14.8 billion in loans, partially financing a total gross merchandise value of EGP 16.5 billion through 4.1 million transactions. In 2025 so far, VALU’s market share stood at around 25%. If we exclude auto loans, that market share goes up to around 27%. More recently, VALU tapped the prepaid card business, ranking first in terms of card growth.

The Listing

What will happen?

Instead of going public through the normal initial public offering (IPO) that companies usually resort to, VALU will be trading on the Egyptian Exchange (EGX) following its direct listing.

However, direct listing alone does not make a stock tradable, which is why EFG Holding [HRHO], VALU’s parent company and the leading investment bank in the region, decided to distribute some of its profits to its shareholders in the form of an in-kind dividend distribution of a partial stake in VALU in lieu of a cash distribution. This marks a milestone in the Egyptian stock market and opens the door for other EGX-listed companies to follow suit the same route, which would create immediate trading liquidity in newly-listed companies.

Following are the details:

- In their ordinary general meeting held on 24 May 2025, HRHO’s shareholders approved the distribution of a portion of HRHO’s retained earnings as of 31 December 2024 amounting to EGP 335,322,346 representing EGP 0.2335 per HRHO share.

- Instead of a cash dividend distribution, a total of 431,546,918 VALU shares (representing 20.488% of VALU) will be distributed to HRHO’s shareholders.

- The distribution will be based on VALU’s book value of EGP 0.777 / VALU share as of 31 December 2024.

- This follows the decisions of VALU’s extraordinary general meetings held on 16 February 2025 and 18 May 2025 to undergo a stock split and to increase the issue capital to 2,106,356,523 shares at a par value of EGP 0.10 / VALU share.

- Eligibility date for the in-kind distribution: 12 June 2025.

- Ex-dividend date for the in-kind distribution: 15 June 2025.

- Allocation is based on the following ratios:

- 3.3273 HRHO shares for each VALU share, which also means

- 0.3005 VALU shares for each HRHO share.

- Trading on VALU shares is expected to commence during the week starting 22 June 2025.

What does this mean for HRHO shareholders?

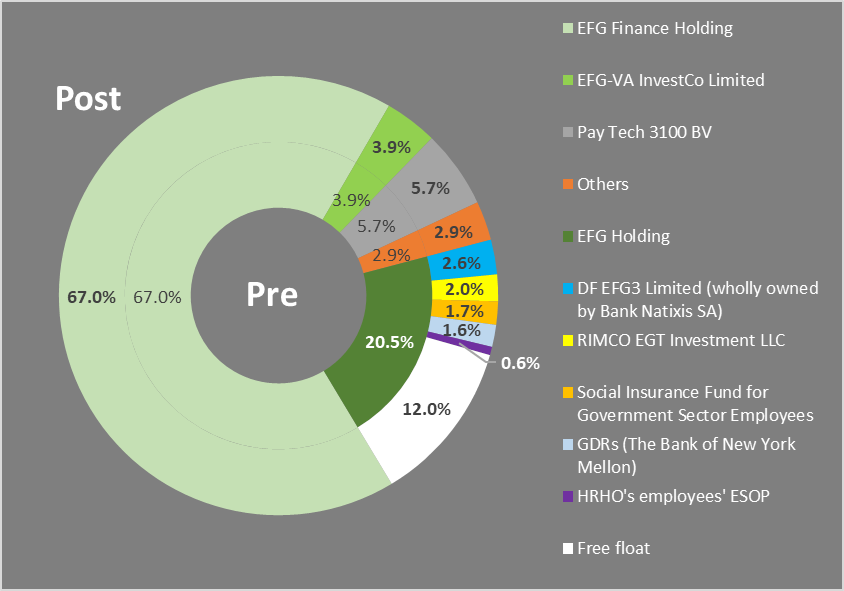

By the conclusion of this transaction, each HRHO shareholder will eventually own a piece of VALU directly. This would technically lead to a lower market value for HRHO, which is the fourth largest constituent of the EGX 30 index.

In other words, think of it as carving out 20.5% of VALU from HRHO’s market capitalization, while having HRHO through its wholly-owned entity EFG Finance Holding retain at least 67% of VALU.

According to our calculation, we estimate that VALU’s free float will eventually be 12%.

Below is VALU’s shareholder structure pre and post transaction, based on our estimates.

Egypt’s Consumer Finance Segment

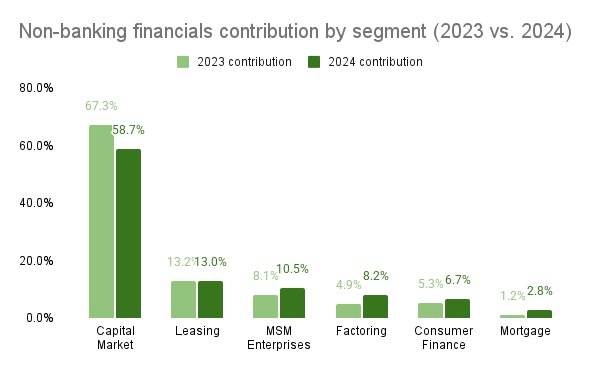

The size of financing within Egypt’s non-banking financial services (NBFS) industry grew 2% YoY in 2024 to EGP 911.5 billion. However, consumer finance has been a steadily expanding segment within the NBFS industry. In 2024, consumer finance recorded a YoY financing growth of 29.6%. Also, its share of the overall NBFS market also increased, rising from 5.3% in 2023 to 6.7% in 2024.

| Non-banking financials financing(EGPbn) | 2023 | 2024 | YoY growth |

| Capital Market | 601.7 | 535.5 | -11.0% |

| Leasing | 117.5 | 118.9 | 1.2% |

| MSM Enterprises* | 72.6 | 95.8 | 32.0% |

| Factoring | 44 | 74.6 | 69.5% |

| Consumer Finance | 47.3 | 61.3 | 29.6% |

| Mortgage | 10.4 | 25.5 | 145.2% |

| Total | 893.5 | 911.5 | 2.0% |

Source: The harvest of FRA 2024

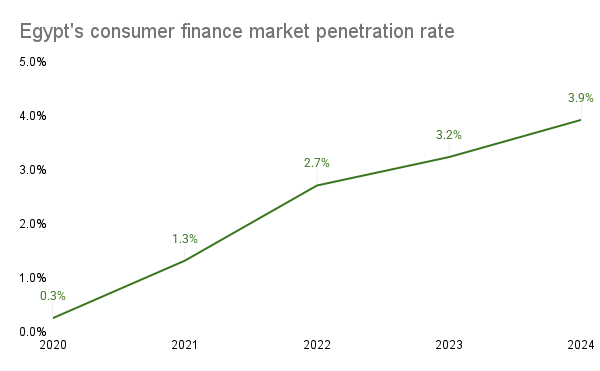

The number of clients within Egypt’s consumer finance segment grew nearly sixteenfold between 2020 and 2024, rising from over 250,000 to more than 4 million. This rapid expansion was driven by growing demand for credit given a growing financial awareness and in view of rising inflation which negatively impacted the purchasing power of Egyptians. As a result, according to our calculation, the penetration rate—as measured by the number of consumer finance clients relative to the total population—rose significantly from 0.3% in 2020 to 3.9% in 2024.

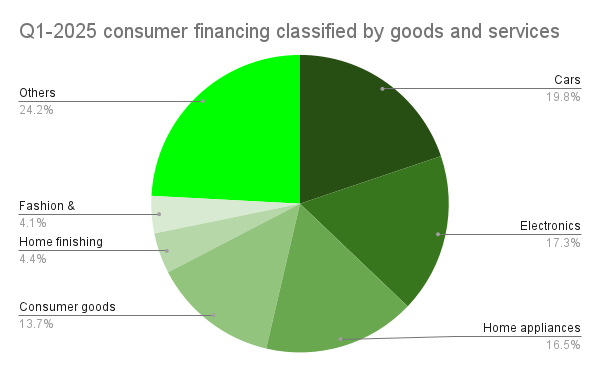

Currently, there are 45 companies licensed to provide consumer finance services in Egypt. According to the FRA’s latest monthly report, consumers primarily seek financing for three key categories: cars, electronics, and home appliances—together accounting for nearly half of total consumer finance demand.

In Q1-2025, the consumer finance segment saw remarkable growth, with the number of clients surging by 188% YoY to 2.3 million (a quarterly figure). Meanwhile, the total value of financing increased by nearly 45%, amounting to EGP 17.5 billion, noting that Q1-2025 is usually the lowest of all quarters.

| Consumer finance KPIs | Q1-2024 | Q1-2025 | YoY growth |

| Number of clients (million) | 0.8 | 2.3 | 188% |

| Total value of financing (EGP billion) | 12.1 | 17.5 | 45% |

How VALU Makes Money?

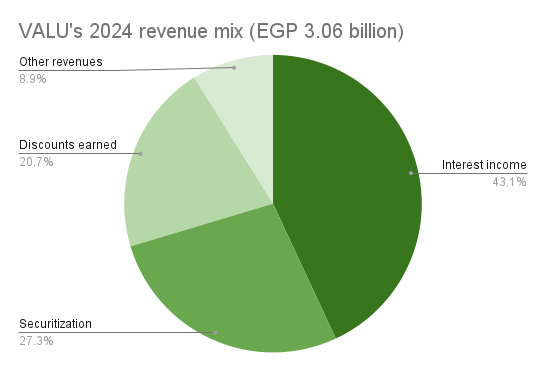

As a consumer finance service provider, VALU generates its revenues primarily by extending credit to individual and business customers. Its core income streams include interest income from consumer finance as well as gains from securitization activities—both in the form of upfront profits and residual surpluses.

Additionally, VALU benefits from discounts earned through supplier arrangements and other revenue sources tied to the nature of its financing operations, such as late fees, prepaid cards, and early repayment fees.

Source: Company reports

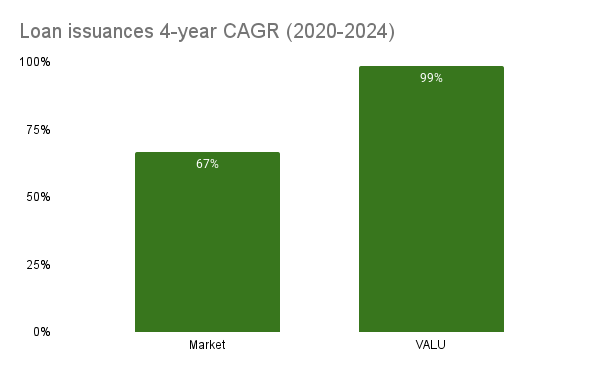

The nature of the consumer finance segment, combined with VALU’s strong brand positioning and equity, led to a robust financial performance and rapid growth. This is evident in the substantial increases in transaction volume, Gross Merchandise Value (GMV), and loan issuances, which have achieved impressive 5-year CAGRs of 137%, 118%, and 116%, respectively.

The Good

VALU is a pioneer in the BNPL space, outgrowing the consumer finance industry

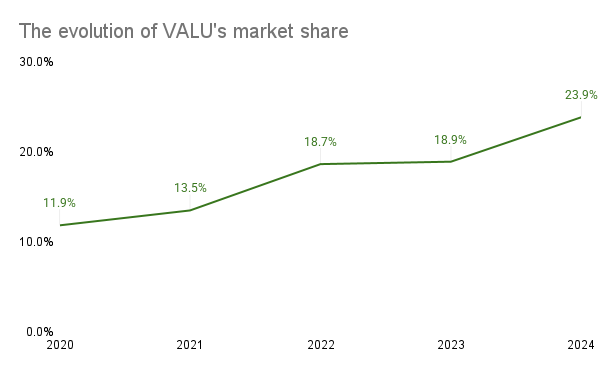

Being a key player in the segment, VALU has been growing robustly, doubling its market share—as measured by the total value of loan issuances—from 11.9% in 2020 to 23.9% in 2024. Moreover, VALU’s 4-year CAGR of loan issuances is around 1.5x the overall consumer finance segment’s.

VALU’s diversified approach resulted in a massive market share growth in a shrinking auto market

VALU tapped into new financing and payments markets, grabbing a considerable market share by offering consumer-friendly and easy financing and payment solutions. In Q1-2025, VALU commanded market shares of 37.5% market share in the prepaid card market as well as 15.2% in the auto market share (vs 2.4% in Q1-2024).

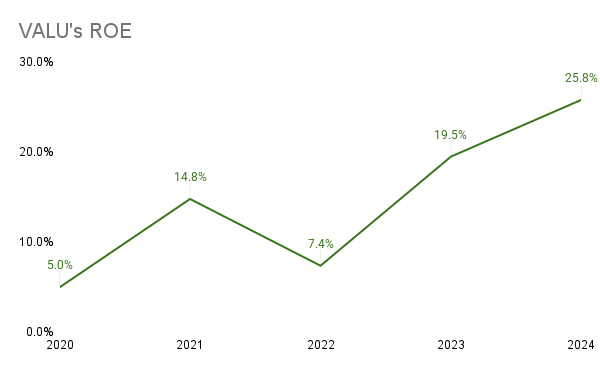

VALU’s growth was reflected in its profitability ratios, mainly ROE

The overall growth in VALU’s metrics, such as the volume of transactions, the total Gross Merchandise Value (GMV), the loan issuances, and the number of merchants, all contributed to the increase in the company’s ROE which grew more than fivefold, rising from 5% in 2020 to 25.8% in 2024.

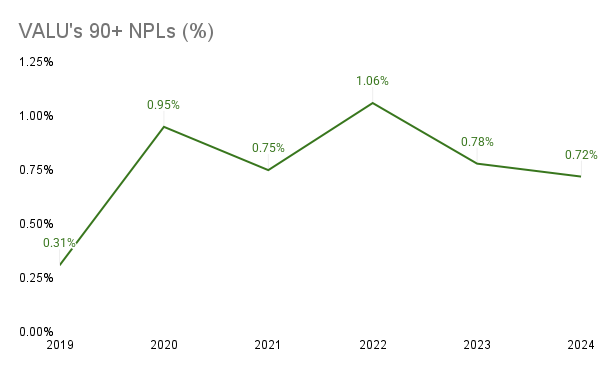

AI-driven risk management to address surging growth, while maintaining a solid risk profile

Artificial intelligence (AI) tools can analyze vast amounts of data, improving credit assessments and fraud detection. This proactive approach helps VALU identify and mitigate potential risks, reducing default rates and enhancing overall portfolio quality.

Despite growing on multiple fronts, VALU has a solid risk profile by maintaining its 90+ non-performing loan (NPL) ratio below 1%. In addition, VALU has a debt-to-equity ratio 4.7x (versus a maximum threshold of 9x as per Egypt’s regulations).

A well-recognized fintech player with a strong brand equity benefiting from the first-mover advantage

Early entry into the market allowed VALU to capture a loyal customer base. The company’s strong brand equity enhances customer trust, drives repeat usage, and reduces customer acquisition costs over time.

A beneficiary of the networking effect, driven by its transaction volume leadership

As a beneficiary of the networking effect, driven by its leadership in transaction volumes, VALU stands to gain exponential value as more users join and interact within its ecosystem. For example, according to management, a typical VALU client completes around 7 transactions per year, while a client using VALU’s prepaid card averages 10-12 transactions per month.

Access to finance through banks and non-banking financial institutions

Access to finance through both banks and non-banking financial institutions (NBFIs) provides VALU with greater funding flexibility and resilience, allowing it to optimize its capital structure, reduce reliance on any single funding source, and potentially secure more favorable financing terms.

A proven track record by an innovative young management team disrupting the industry

The proven track record demonstrates the team’s ability to execute ambitious strategies, respond to market shifts, and create value through innovation.

Investment Catalysts

Regional expansion to drive growth

VALU’s expansion plans shall leverage its established products, services, and operational expertise to capture additional demand and diversify its revenue streams. VALU is currently in the process of penetrating the Jordanian market.

Declining interest rates in Egypt to reduce funding cost

Declining interest rates shall improve profitability and enable more competitive lending rates to customers. Lower borrowing costs can also encourage VALU to expand its loan portfolio and take on new growth opportunities with greater financial flexibility.

Declining inflation rates in Egypt to drive demand

As inflation cools, albeit still at elevated levels, consumers may feel more confident in taking on new credit, which could support VALU’s growth. This is especially true in view of low real wage growth rate.

Utilizing current leverage buffer to support further growth

VALU can utilize the buffer between its current debt-to-equity ratio of 4.7x and the threshold debt-to-equity ratio of 9x to support further growth.

Any potential acquisition of VALU could drive growth further

Being a target for acquisition enables VALU to expand its customer base and unlock operational synergies. Acquisitions can also provide access to new markets, technologies, or capabilities, strengthening the company’s competitive position and supporting long-term value creation.

Key Risks

A market with low barriers to entry with rising competition from new entrants

Egypt’s consumer finance market has low barriers to entry, which poses a risk that can lead to pricing pressure, shrinking profit margins, and potential erosion of market share. This can raise investor concerns about the sustainability of growth and profitability, potentially impacting VALU’s valuation. However, VALU can differentiate itself—through its brand equity, technology, or service quality.

No cash dividend plans in the foreseeable future

The absence of cash dividend plans in the near future can be a concern for income-focused shareholders who rely on dividends as a source of return. So, from a market perception standpoint, withholding dividends can negatively affect investor sentiment. However, VALU’s plan is to reinvest retained earnings into the business, further fueling growth, which would be a sound long-term strategy if effectively executed.

Potentially a limited free float percentage

A potentially limited free float of 12% implied a total free float market capitalization of less than EGP 2 billion (based on the IFA valuation). This can lead to a relatively low trading activity on the stock. Such reduced trading liquidity may also make it harder for investors to trade the stock without impacting its price significantly. It also tends to discourage institutional investors who require sufficient float to build or exit positions efficiently.

The risk of existing pre-transaction shareholders selling off

A significant sell-off by early investors can lead to a sharp decline in the stock price, especially if the float is already limited. This can negatively affect market sentiment and deter new investors who may fear continued downward pressure from this sell-off overhang.

If interest rates reverse direction higher or rate cuts come in slower than expected

Since the consumer finance segment relies heavily on borrowing, higher interest rates or slower- than-expected rate cuts mean a higher-than-expected cost of funding. This can compress VALU’s profit margins and reduce its ability to offer competitive lending terms. On the demand side, consumers may become more hesitant to take on credit, leading to slower loan growth.

If VALU approaches the maximum allowed leverage threshold

This could limit VALU’s ability to raise additional debt to support future growth or absorb financial shocks. Operating near the regulatory ceiling also signals elevated financial risk, which may concern investors.

If the market dries up with demand for securitization faltering

Faltering demand for securitization could significantly impact VALU’s liquidity and funding strategy. Securitization is often a key tool for converting outstanding receivables into immediate capital (cash), and a slowdown in demand would limit this avenue, potentially forcing the company to rely more heavily on costlier or less flexible funding sources.

]]>By: Amr El Alfy, MBA, CFA

Looking Back — and What’s Changed

About a year ago, we advised investors to avoid City Lab [CILB] because of its small size and a strategy that is yet to be proven. Fast forward to today, and the company—now called Premium Healthcare Group [PHGC]—is undergoing a significant transformation. You can think of it as “City Lab 2.0.”

So, what’s happened since then?

In November 2024, PHGC shared a study outlining its expansion plans in Egypt as well as outside Egypt. It’s targeting Saudi Arabia, the UAE, and Jordan. We saw two main parts to this plan:

- Local expansion: By acquiring other operating businesses including labs in Egypt.

- Regional expansion: Through partnerships with labs in each new market.

And now, PHGC is moving forward with that plan through a massive capital increase—growing its paid-in capital by 29 times, from EGP81.5 million to EGP2.36 billion. Most of that increase is coming through a debt-to-equity swap.

What’s Behind the Capital Increase?

Over the past year, PHGC acquired several businesses. It paid for some in cash, but the rest (worth EGP1.32 billion) was recorded as “dues to related parties”—essentially money it owes to the sellers of those businesses.

To settle that debt, PHGC is issuing new shares. The sellers will receive PHGC shares in return for their ownership in the businesses acquired. So instead of being creditors, they’ll now become shareholders.

Why Investors Are Asking Questions?

This capital increase is huge—and it changes the game for current and potential investors. Many of you have asked whether you should participate or not. Before you decide, here are a few key points to consider.

The Most Important Question: What If I Don’t Subscribe?

If you’re eligible to participate in the capital increase but choose not to, your position will likely take a big hit.

Here’s why:

The number of new shares being issued is 28 times the existing number, and they’re being offered at just 10% of the stock’s market price before the ex-right date.

So, you’re left with two choices:

- Subscribe to the capital increase to protect the value of your investment.

- Sell your rights, but keep in mind those rights have dropped about 70% since they started trading. You’d be selling at a steep loss.

But What If My Portfolio Is Already Down?

Many shareholders are seeing losses in their portfolio. But those losses are likely due to the drop in the value of the rights—not necessarily the stock itself.

Here’s how to think about it:

- You might be up on the PHGC shares you originally bought.

- But you’re probably down on the PHGCr rights you received.

To avoid locking in those losses, subscribing is your best option—it helps protect the total value of your holdings.

What Are the Risks?

There are a few important things to keep in mind:

- PHGC is still listed on the SMEs stock market (formerly Nilex), which is more volatile and less liquid than the EGX main board.

- The company plans to move to the EGX after this capital increase—but it’s unclear how the stock will perform post-transfer.

The owners of the acquired businesses (who are subscribing with their dues) will own most of the new shares. While 25% of their shares will be locked up for 2 years, they’re free to sell the remaining 75%, which could pressure the stock price when those new shares start trading.

So Why Is PHGC Raising All This Money?

The simple answer: to fund its expansion strategy.

Here’s the breakdown, based on PHGC’s 2024 financial statements:

- EGP1.32 billion (58%) is being paid in kind—by settling the money owed to sellers of the acquired businesses.

- EGP963 million (42%) is being raised in cash—from PHGC’s existing shareholders who choose to subscribe.

Key Dates to Remember

- 6 May 2025: PHGC traded ex-right (buying the share no longer comes with the right to subscribe).

- 8–29 May 2025: The tradable right PHGCr is being traded on the market.

- 8 May – 3 June 2025: Capital increase subscription window is open.

Can You Make a Profit by Buying the Rights Now?

To answer that, compare what you’d pay (right + subscription cost = EGP0.11/share) to the market price of PHGC.

- As of last Thursday, PHGCr was “in the money”—meaning you could profit if PHGC stays above EGP0.11/share.

- If the right’s price increases, the profit margin narrows.

It’s key to monitor the total payoff of the right, not just its market price.

Your Options — Based on Your Situation

You can also download this sheet to model different scenarios based on your own cost basis.

If You Bought Before 6 May (e.g., cost basis = EGP1.04/share)

- You now have rights equivalent to 28x the number of shares you had.

- You’re likely up 93% on your shares, but down 69% on the rights—net portfolio down ~49%.

- Recommended: Subscribe to reduce your cost to EGP0.132/share.

- Break-even: PHGC would need to drop over 48% for you to start losing money.

If You Bought After 6 May (e.g., assuming cost basis = EGP0.150/share)

- You don’t have any rights.

- You’re likely up ~70% on the stock.

- Recommended: Consider taking profit if you’re happy.

- Break-even: PHGC would need to drop over 41% for you to start losing.

If You’re Not a Shareholder (cost basis = EGP0.010/right)

- You can buy PHGCr and subscribe at EGP0.10/share.

- If you do, you’d be up ~132% on the portfolio.

- Recommended: This could be a good trade if PHGC stays above EGP0.11/share.

- Break-even: PHGC would have to drop more than 57% for you to start losing money.

What About the Company’s Valuation?

We haven’t done a full valuation exercise yet, given PHGC is still on the SMEs board and the performance of the merged group isn’t fully known.

But we do know this:

- PHGC’s 2024 consolidated net earnings = EGP241.5 million

- At EGP0.255/share, PHGC’s market cap = EGP6.03 billion → P/E = 25x

- That’s much higher than its peer, IDHC, which trades at 10x.

- At EGP0.11/share, the implied P/E is 10.8x—much more reasonable.

Bottom line: The key will be whether PHGC delivers strong growth after the capital increase.

Final Thoughts

Here’s how we’d sum it up:

- Bought PHGC before 6 May? → You should subscribe to protect your investment.

- Bought PHGC after 6 May? → If you’re in profit, consider taking it by selling.

- Not a shareholder yet? → This might be an opportunity if you’re comfortable with risk.

Keep in mind: Subscribed shares won’t be tradable right away—you’ll be exposed to market moves in the meantime.

Keep in mind: Subscribed shares won’t be tradable right away—you’ll be exposed to market moves in the meantime.

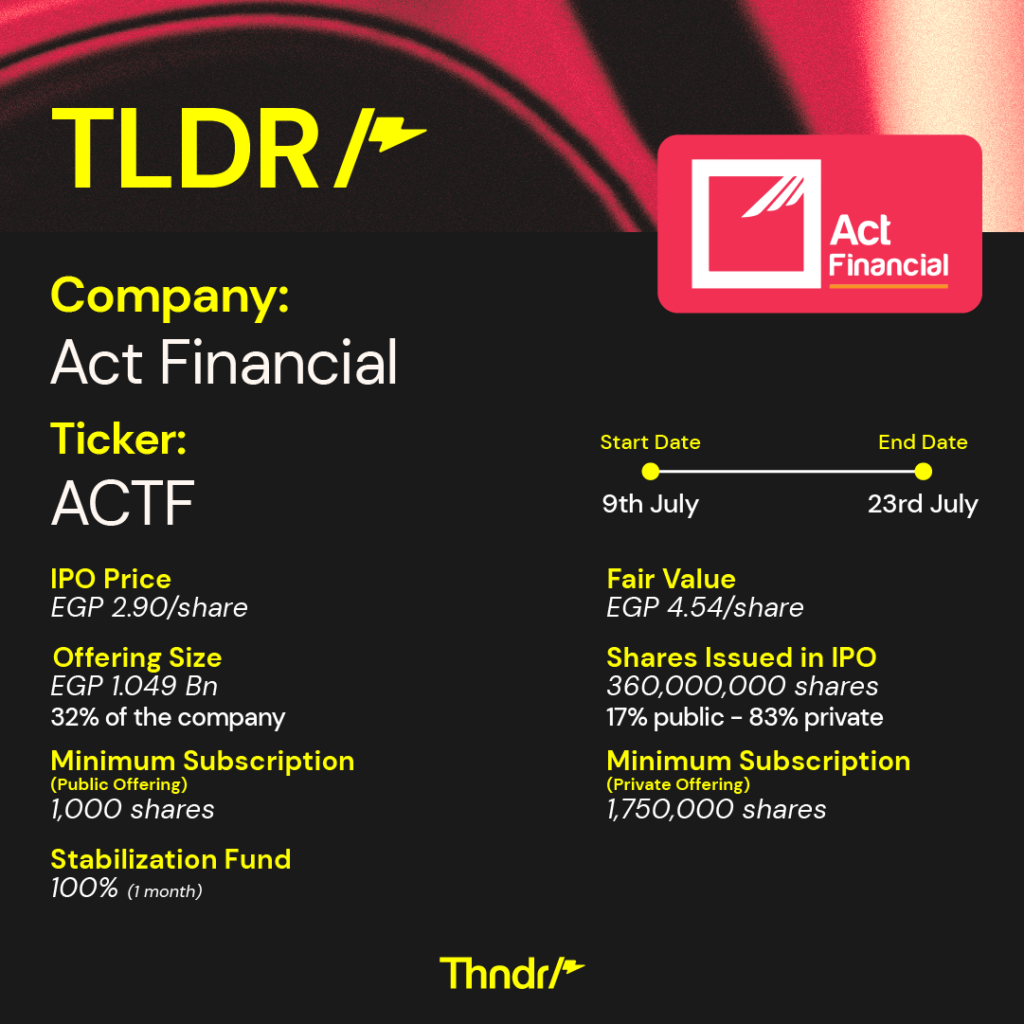

Investing in the Act Financial IPO on Thndr is a risk-free investment (read more below on why we say this!) that can yield returns for everyone from first timers to savvy investors who are looking to make their first mark with this IPO.

If this sounds like a potential opportunity for you (it should!) we’ll guide you on all the ‘must-knows’ of this IPO.

To start investing – you need to know the company – so, who are Act Financial?

Act Financial is an Egyptian investment company founded in 2015, focusing on the Egyptian stock market. They follow an active investment approach – which means that they buy a stake in a company with the aim of influencing its decisions, unlike a passive investor who invests and sits back.

Here’s what really excites us about this IPO:

The upcoming IPO for Act Financial is an exciting opportunity several reasons:

- It’s the first IPO Since February 2022: We are eager to see if this marks a new era in the Egyptian Stock Market following the mega Ras El Hikma deal.

- It’s a different way to invest in stocks: You can be part of a company that invests in publicly listed companies and owns an influencing stake in those companies.

- And most importantly it’s a ‘risk-free-your-money-guaranteed’ type of IPO.

Is this investment for me?

This IPO is best suited for two types of investors:

- I’m a newbie investor: If you’re relatively new to the investment space then this is the easiest way to start getting into the playing field, with a risk free opportunity (keep reading to know more on this). This IPO will allow you to learn more about the stock market and how to make money.

- Active investment-seekers: If you’re seasoned in the stock market, then you know you need to do your research. Every new IPO presents a new investment opportunity. However, similar to any investment in a company you make, it is important to understand the business model, growth potential, quality of leadership and financial health. It’s equally important to determine whether it is fairly valued, undervalued or overvalued. We list out below the main metrics we believe you should review.

What the beginners need to know:

First off it’s important to understand what an IPO is, and how it works – we recommend you you go through our light read here on the Thndr learn platform to do this.

Yes, we mean it when we say ‘risk-free’: Introducing you to the stabilization fund.

Act Financial has a 1-month stabilization fund that covers 100% of the IPO retail offering. This means that on day 30 of the IPO, you can sell your shares for the price you bought them at. If you bought them for EGP 2.9/share for example, and their price fell to EGP 1/share, you can sell them back for EGP 2.9/share. Also, to make this even more compelling, Thndr will be waiving transaction fees if you sell in the stabilization fund (doesn’t get more risk-free than this!)

Here’s how it works:

- Will be sending out an email to the users if the price falls below the IPO Price (2.9 EGP ) within the 30 days of the stabilization fund period with the instructions required.

- After 30 days, if the price of the stock is below the IPO price , orders placed for the stabilization fund will be executed with the initial IPO price (2.9) and the amounts will be added to your wallet,

- Note that this is only limited to users who subscribed in the IPO as any traded quantity post the trading start date will be excluded.

What to watch out for?

- Oversubscription: It is very common for IPOs to be oversubscribed, meaning that the demand from investors to buy shares in the IPO exceeds the number of shares offered in the IPO. Allocation of shares is on a pro-rata basis, meaning that the investor’s order sizes are divided by the degree of oversubscription, where you’ll know your final share count. This might reduce the size of the investment you intended to go for. In case of oversubscription, the extra money that wasn’t used to purchase shares will be refunded to your Thndr wallet. You can withdraw this money to your bank account or invest it on Thndr.

Let’s take an example: If you place an order for 20,000 shares but the IPO is oversubscribed 20 times, you will only receive 1,000 shares (1 over 20 of what you ordered, based on the oversubscription rate).

It’s important to know that this is very common during an IPO, and bound to happen to the majority of investors – setting your expectations on this will help you manage your expected returns better.

While oversubscription is common, it’s also important to be aware of the possibility of undersubscription. If the IPO is undersubscribed, you might end up needing more money than you originally planned for.

For example: If you place an order with 4x your money, and it ends up being subscribed by only 2x, you would need to deposit fund in your wallet equivalent to the difference on the first trading day or sell your shares. This is a crucial consideration to keep in mind as you plan your investment strategy for the Act Financial IPO.

However, you also need to take watch out for undersubscription

- Understanding the risks of time: Because this IPO comes with the perk of the stabilization fund, it also comes with the risk of missing the deadline to be part of it in case the stock price falls below IPO price (like we said above, this is on day 30). So, make sure you mark your calendars! Additionally, when you enter the IPO you need to watch out & plan for your money being locked up until the subscription period is over, again in case the stock price falls below the IPO price and you decide to wait until day 30 and redeem your shares back to the subscription fund – so, you need to be wary that your money-back guarantee is not immediate, and will take 30 days to be released. In other words, everything risk-free about this IPO comes with a time restriction.

I’ve made it till here & I’m hooked. Now, how do I start?

Subscription in the public offering starts from 9th of July till the 23rd of July; to participate in Act Financial’s IPO, follow these simple steps:

- Download the Thndr app and open an investment account (we’re assuming you already have though!)

- Top up your wallet – We recommend making sure your wallet is set and ready for when subscription opens – so make sure to get this done early on!

- Place your order! Straight from the Thndr app just search ‘ACTF’ & submit a buy order for no less than 1,000 shares & no more than 1,750,000 shares

If you’re an active investment-seeker – dive in:

As a more experienced investor, this is a refresh on what we recommend you need to review before taking further action in this IPO:

- Industry

- Outlook

- Growth

- Barriers to Entry

- Company

- Historical Performance

- Management Quality

- Company Plans & Products

- Competitive Landscape

- Valuation

- Discounted Cash Flows

- Multiples

If you’re not on Rumble, make sure to subscribe where you can find information on all the key factors mentioned above & a recent exclusive interview with Mostafa Abdelaziz and Karim Neema, Co-founders and Managing Partners at Act Financial.

For more in depth details we also have the IPO prospectus – which you can review here, and the company’s IPO teaser which you can view here.

If you’re interested in participating in the private offering, please fill in this form to complete the offline process

The minimum subscription is 1,750,000 shares and it’s important to note that there is no stabilization fund. Once the form is filled, we’ll reach out with more details and exact process. Please note that the deadline for the private offering is earlier, and ends on July 18th.

If you have any questions for us regarding the IPO, we will be conducting a Live Q&A Webinar soon, please put your questions in this link here and we will be answering them.

]]>