Built from the questions, conversations, and needs we heard across our community, we’re excited to introduce the Thndr Zakat Calculator.

This Calculator has been reviewed and approved by Dr. Magdy Ashour, Former Scientific Advisor to the Grand Mufti of Egypt.

Last Ramadan, we noticed something important. Zakat questions kept coming up from our users. Not just as a general question, but as a real point of confusion:

- How do I calculate Zakat on stocks?

- Do savings products count?

- What about gold funds?

- What if my money is spread across multiple assets?

As more people began building wealth across different Thndr products, one thing became clear: calculating Zakat accurately can get complicated, and at times, overwhelming.

So we listened. And we built a simpler way to do it. At Thndr, we believe managing your finances should feel simple, and that includes fulfilling your religious obligations with confidence. That’s why we asked ourselves: what if Zakat calculation could be done easily, directly inside the app?

What is the Zakat Calculator?

The Zakat Calculator is a tool embedded within the Thndr app in My Hub that helps you calculate your Zakat based on Islamic principles. The best part? It automatically pre-fills your Thndr portfolio data, so you’re already halfway there before you even start.

How does it work?

Step 1: Open the Calculator

The calculator calculates based on the Hijri year by default. But if you are following the Gregorian year in your Zakat, just choose it, and we’ve got you covered.

The calculator shows you the current Nisab threshold (the minimum wealth required for Zakat) based on the latest gold price. This assumes that your reached the Nisab (your Hawl started) exactly one year ago.

Start your Hawl on a different date? You can customize this! Tap on today’s date to select when your wealth crossed the threshold. This also allows you to calculate Zakat for any past year, not just the current one.

Your Thndr wallet balance, Saving Clouds balance, and stock portfolio are already pre-filled for you to make your experience easier. You’ll just need to add assets you own outside Thndr.

Step 2: Add Your Assets & Liabilities

Enter your wealth across 8 categories, and don’t worry, your Thndr assets are already prefilled:

- Cash & Balances: Bank accounts, savings, physical cash

- Investments: Stocks & Mutual Funds

- Bank CDs: Certificates of deposit

- Gold: Coins, bars, or jewelry

- Silver: Coins, bars, or jewelry

- Real Estate: Properties you own

- Lendings: Money you’ve lent to others

- Business Assets: Inventory, receivables, business cash

- Debts: Money you owe (this reduces your Zakat amount)

Purpose-based Calculation

Different assets have different Zakat rules depending on their purpose. Be aware to enter the purpose for each investment, Thndr assets and external assets, in the calculator. The calculator guides you through the right treatment for each asset type.

Step 3: Get Your Result

Tap “Calculate Zakat” and instantly see your Zakat amount with a full breakdown. If your wealth is below the Nisab threshold, we’ll let you know that you’re not obligated to pay Zakat this year.

Features you’ll love

Custom Nisab Date — Set the exact date when your wealth first reached Nisab to calculate Zakat for any year — past or present.

Smart Pre-filling: Your Thndr investment wallet, Clouds savings, and complete stock portfolio are automatically imported. Just add assets held outside Thndr.

Purpose-Based Calculation: Different assets have different Zakat rules depending on their purpose. The calculator guides you through the right treatment for each asset type.

Hijri or Gregorian Year: Choose to calculate based on the Islamic lunar year (2.5% rate) or the Gregorian year (2.577% rate).

The preferred basis for calculation is the Hijri year. However, if someone needs to calculate using the Gregorian year, it is permissible.

Quick Facts

- Nisab Basis: 85 grams of 21K gold

- Zakat Rate: 2.5% (Hijri) or 2.577% (Georgian)

- Hawl Requirement: Your wealth must stay above Nisab for one full continuous year

Ready to calculate your Zakat?

Open the Thndr app and find the Zakat Calculator to get started. It’s the easiest way to fulfill your obligation while keeping all your financial data in one place.

For more details on how the amount is calculated, please visit the Zakat Calculator Support page.

Have Questions?

If you need any assistance, our in-app support team is ready to help. Just reach out, and we’ll guide you every step of the way!

Watch instead: A must-watch conversation with CEO Ahmad Hammouda and Amr El Alfy breakdown the GOUR IPO!

This is all you need to know about Egypt’s first IPO in 2026: The country’s leading premium grocer.

30 January 2026

Amr Hussein Elalfy*

The Story

Gourmet [GOUR] is one of Egypt’s most established food retailers, built around a simple idea: offering high-quality food to customers who care about what they consume. What began as a family-run business has grown steadily over time into a trusted brand, with a loyal customer base and a clear focus on quality rather than rapid, unfocused expansion.

The company serves a specific segment of consumers whose spending tends to remain more stable even during economic slowdowns. This positioning has helped Gourmet maintain resilience compared to more mass-market retailers that are more exposed to swings in consumer purchasing power.

A key part of Gourmet’s model is that it produces a meaningful portion of what it sells through its own food solutions arm. This gives the business greater control over quality, costs, and supply, while reducing exposure to imports. In a market where currency and supply-chain disruptions can be common, this level of control has become an important advantage.

Over the past two years, Gourmet has gone through a clear operational turnaround. After a period of losses, the company returned to profitability in 2024 and has continued to build on that momentum. Strong cash generation has allowed Gourmet to fund store expansion, invest in the business, and pay dividends without relying heavily on debt.

Looking ahead, Gourmet’s growth plans are focused and disciplined. The company intends to expand its store network in key areas such as East and West Cairo, operate larger and more efficient formats, and grow its in-house and private-label offerings. At the same time, loyalty programs and better use of customer data are expected to deepen engagement with existing customers.

With this IPO, Gourmet becomes the first food retailer to list on the main Egyptian Exchange. For investors, this provides differentiated exposure to Egypt’s consumer sector through a business with a strong brand, controlled growth, and a long-term mindset.

As with any investment, risks remain – including competition and the niche nature of the segment Gourmet operates in. That said, the company’s brand strength, control over its products, and consistent cash generation give it a solid foundation as it enters the public market.

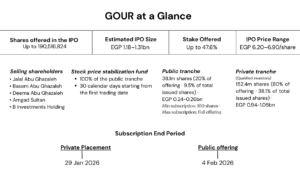

The IPO

GOUR will go public on the main exchange through a public and private offering with the following details:

Source: Prospectus, Rumble Research

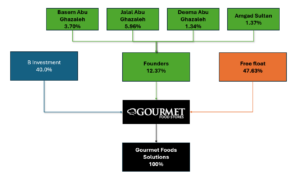

Shareholder Structure (Pre-IPO)

Source: Prospectus, Rumble Research

Shareholder Structure (Post-IPO)

Source: Prospectus, Rumble Research

Background

2006: A Premium Retail Brand Was Born

- GOUR was established in 2006, initially supplying high-end hotels and business clients in Cairo with quality meat and specialty food products. This early success led the company to open its first premium retail store in 2008, offering a curated selection of fresh, locally produced, and imported goods not commonly found in traditional supermarkets. Since then, GOUR has continued to grow while focusing on quality, reliability, and customer experience.

2015: Vertical Integration Strategy Adopted

- In early 2015, rising devaluation pressures on the EGP forced GOUR to pivot from importing and distributing final products to outsourcing and manufacturing. This shift introduced Gourmet Foods Solutions (GFS) to the market, a “Handcrafted by Gourmet” production line operating in two factories (kitchens), one owned and another leased.

2018: B Investments Steps In

- In 2018, EGX-listed B Investments Holding [BINV] acquired a significant stake in GOUR (40% initially) before increasing it through a follow-on capital increase (to 52.9%). This step reflected BINV’s confidence in GOUR’s business and its potential to grow as a leading premium food retailer in Egypt.

2020: The Up Spike

- Like basically all other businesses, GOUR’s nationwide expansion was disrupted by COVID-19 in 2020 which slowed momentum at first in its walk-in stores due to nationwide lockdown. However, the silver lining was for GOUR’s business to go online. Indeed, GOUR launched its digital app to cater to its clientele who preferred online shopping to in-store shopping. Also, the new app helped GOUR capture customer data and refine offerings personalization for customers.

- To capture growing demand, GOUR invested heavily in acquiring three delivery hubs around Greater Cairo to be closer to its customers. But after lockdown restrictions were lifted, customers began going back to in-store shopping. Thus, overspending resulted in losses in 2021 and 2022, having expanded aggressively in the delivery segment with revenues not picking up as fast as expected.

2022: The Turnaround

- GOUR’s shareholders, led by BINV, decided it was time to turnaround the business. In 2022, GOUR hired a veteran team led by Michael Wright with vast regional retail experience in the MENA region across many household names.

- Under the new management team’s oversight, revenue maximization and cost reduction measures helped restore profitability, delivering net profits of EGP31mn in 2023 and EGP135mn in 2024, with more than EGP200mn estimated in 2025. This turnaround story was driven mostly by organic growth with zero net additional stores in 2024 and 2025.

2026 & Beyond: The Next Chapter

- GOUR’s vision is to continue growing and unlocking additional value within its existing business. This will be done through two pillars:

- An organic pillar through increasing the retail area of existing locations to improve customer experience and support higher basket sizes and better traffic flow, while maintaining its premium positioning.

- Expanding its presence across East and West Cairo, while remaining open to selective opportunities in Downtown Cairo if attractive locations become available.

How GOUR Makes Money

Premium retailing, in-house products & e-commerce

- Premium Retailing

GOUR targets niche, higher-spending customers rather than competing with mass-market retailers, which limits direct competition. The company also operates three seasonal stores in the North Coast, supporting its geographic diversification and exposure to premium consumer demand. - In-house Products

Gourmet Food Solutions (GFS), a wholly owned subsidiary of GOUR, is its in-house food production and processing unit. GFS cuts the middle-man by making fresh and ready-to-eat products like sandwiches, bakery items, ready-to-eat meals, and salads. GFS provides its products to Gourmet’s stores, Gourmet’s online platform, and selected business clients. Regular retail products usually have a 20-30% gross margin, while Gourmet’s in-house and private label products have a higher margin of about 50% because they are exclusive and premium. - E-Commerce

GOUR’s e-commerce channel sells products directly to its customers on its website and mobile app. This online channel helps GOUR reach more customers who can make more orders from the comfort of their home, while GOUR uses the customer data to improve its product offerings. Today, e-commerce and call centers contribute about 35% of GOUR’s total sales with room to grow further.

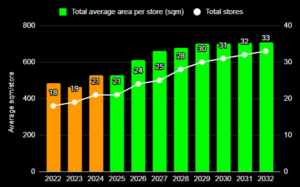

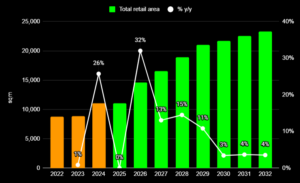

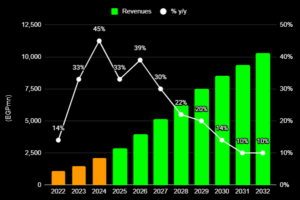

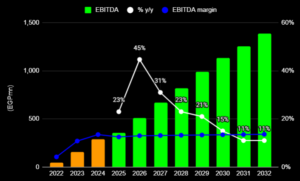

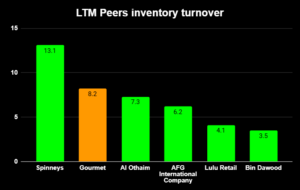

GOUR in Charts

Source: B Investments Holding Earnings release, Rumble Research

Source: B Investments Holding Earnings release, Rumble Research

Source: B Investments Holding Earnings release, Rumble Research

Source: B Investments Holding Earnings release, Rumble Research

The Good

- First of its kind on the EGX

- Gourmet’s IPO marks the first time for the EGX to see a retailer in the F&B industry listed on the main exchange. For investors with an appetite for the retail business, their only available option is GOUR, especially given its much better margins versus regional peers.

- Operating in a segment with relatively inelastic demand

- GOUR operates within a niche market, targeting the affluent segment of the society. This helps smooth out any earnings volatility in the case consumer purchasing power softens. So, while some consumers may decide to shift from premium products toward more affordable alternatives, GOUR’s clientele is loyal in view of its premium-quality products and minimal impact on their spending habits despite any economic downturn.

- Asset-light, lease-based business model

- GOUR’s lease-led expansion strategy lowers upfront capital requirements per store, supporting an average rollout of 2–3 stores annually. The company targets store sizes of at least 800 sqm. Fit-out costs average EGP60–80mn per 1,000 sqm (implying a cost of EGP60-80k per sqm).

- However, in mall locations, GOUR typically bears around half of that cost, with landlords funding the rest. This is because GOUR has become a partner of choice for many real estate developers. This allows GOUR to expand more rapidly and achieve attractive returns for new stores.

- For instance, the last 2 stores GOUR opened had a payback period of 1 year.GOUR’s lease tenors average nine years which enhances cash flow visibility. Leases entered into with real estate developers usually have both fixed and variable components. The fixed component is a minimum guarantee lease payment, which is fairly easily surpassed by the variable component (a revenue share model).

- Vertical integration driving margin resilience

- Logistics & supply chain risk management: Given that GFS primarily serves GOUR, the company maintains tight control over inventory levels, reducing reliance on external suppliers. This vertical integration has supported higher inventory turnover ratio relative to peers.

- Limiting imports: GOUR’s transition toward local manufacturing reduced FX-related cost pressure while preserving its premium positioning, boding well for margins.

- Outsourcing equipment: For products requiring specialized, capital-intensive equipment, GOUR outsources production through rented manufacturing lines at third-party facilities. This strategy supports higher profitability while hedging against changes in consumer demand.

Source: Koyfin, Rumble Research

- Sustainable cash flows with high earnings visibility

- Short payback period: GOUR’s new stores benefit from a short payback period, typically recovering their investment in less than one year. This demonstrates how the company uses its capital efficiently and ensures that new stores will be cash flow positive quickly. This highlights the resilience and attractiveness of GOUR’s business model.

- Short cash conversion cycle: GOUR operates with a negative cash conversion cycle (CCC) of around 2 days. With more than 50% of sales paid using credit cards, GOUR receives cash from customers before supplier payments are due. This enables the company to fund expansions internally without having to resort to a high level of leverage while also paying cash dividends.

- Experienced management and an active institutional shareholder

- GOUR’s new management team has turned two years of losses into a profitable business. The management team behind this turnaround story, led by Micheal Wright, comes from a regional retail background with a strong track record in many household names, including Bin Dawood in Saudi Arabia and Spinneys in the UAE, Qatar, Egypt, and Lebanon.

- The management team brought onboard by BINV is contracted to remain with GOUR through 2027. However, there is a 5-year ESOP program (expected to be around 5% of GOUR’s shares) that will help retain the management team and other key members within GOUR through 2030.

Key Risks

- Limited and niche market segment

- GOUR’s market share remains limited within Egypt. With projected 2025 revenues near the EGP3bn mark, GOUR’s market share in Egypt’s F&B segment could be well below 5%. GOUR’s total available market (TAM) is constrained by its premium business model targeting quality-conscious consumers, limiting its audience to those with higher purchasing power.

- Limited access to digital retail channels

- Lately we have seen logistics companies offer groceries through their digital channels, like Talabat and Instashop. These companies would definitely expand GOUR’s reach, yet they only contribute around 5% of revenues–a strategic decision by GOUR to safeguard its profitability margins.

- On the other hand, online competition is intensifying. For instance, Breadfast, Egypt’s largest digital food and beverage retailer, could represent a key online competitor to GOUR. Breadfast operates through a fully-digital model, with no physical retail stores, selling exclusively through its mobile application and supported by its own network of delivery hubs.

- Similar to GOUR, Breadfast has developed product lines under the “Made by Breadfast” brand, while also selling white-label products for third parties for higher margins, a model GOUR does not follow. Both companies rely on owned delivery infrastructure to control quality and fulfillment.

- A limited number of SKUs

- The average stock keeping unit (SKU) for the retail businesses in Egypt is usually between 50,000-60,000 SKUs. GOUR has an estimated total of 11,000 SKUs, with 1,200-1,500 SKUs exclusive private labels made by Gourmet.

- This is a key risk because a limited product range deprives customers from variety which can lower the value of each shopping basket.

- Indirect FX exposure but manageable

- GOUR does not have direct exposure to FX as it imports its products from local suppliers. However, GOUR is somehow exposed to a stronger FX rate which could make its imported products more expensive for certain customers. This is quite important absent any FX inflows.

- However, the fact that GOUR operates in a niche market segment that is less vulnerable to a weaker local currency helps mitigate such risk.

- Also, GOUR’s product positioning allows it to pass on higher costs to consumers, though this may weigh on volumes.

Investment Catalysts

- Active shareholder with clear value-creation agenda

- BINV, the company’s major shareholder, still sees untapped potential growth for GOUR. Indeed, BINV expects GOUR’s revenues to double in the next three years, further expanding its market share.

- This is evidenced by BINV’s strategic decision to only undertake a partial exit on only a quarter of its holding (13% of its 53% stake). This should assure new GOUR investors that at some point of time in the future BINV will be looking to monetize its remaining 40% stake at a higher valuation level.

- In other words, BINV is GOUR’s active investor looking to maximize shareholders’ value.

- Successful execution of store expansion plan

- More stores down the aisle: GOUR’s expansions will mainly be in East and West Cairo, currently preparing two stores (potentially three stores) for 2026.

- The G17 store is destined to start operations after Ramadan, while the Midlane is expected to start operations after summer between September and October 2026.

- These new stores will attract more consumers, driving revenue growth further and hence profitability driving growth.

- Bigger space stores: While it was the management’s strategy to increase the number of stores, it’s also their plan to increase their sizes. Having bigger stores allows GOUR to have its kitchen/bakery in the same location, thus minimizing costs. Also, in big stores they have opportunities to innovate and increase their services.

- This aligns with GOUR’s strategy to maintain its geographic footprint as they plan to replace small size stores with larger ones of at least 800 sqm at the same locations.

- Anchoring customers through loyalty programs

- Loyalty programs: GOUR’s loyalty program helps the company build stronger relationships with customers by encouraging repeat purchases and higher visit frequency. It also allows GOUR to collect valuable data on shopping behavior, which can be used to improve product selection, pricing, and promotions.

- Over time, this supports more stable revenue, better inventory planning, and more efficient marketing spend.

Mobile network partnerships: GOUR’s partnership with Orange has been positive, increasing sales without any expenses. Orange provided its Premier clients discounts at GOUR stores through their collaboration. - This brings more customers without increasing selling and marketing expenses.

- Consistent cash dividend payout down the road

- Unlike a few years ago, GOUR’s business model displays today high cash flow visibility. This could mean there will be potential dividends payouts. GOUR’s management intends to pay out dividends in the range of 50-75% of net income.

- An acquisition target by financial or strategic investors

- With BINV retaining a 40% stake in GOUR, this opens the door for potential M&A deals involving GOUR. BINV will be looking to exit GOUR at one point of time in the future, and ideally they will be doing so at a valuation higher than the IPO price, which would act as a floor, in our opinion. This will help the stock re-rate higher after listing.

* Helped in writing this article: Abdelkhalek Mohamed, Equity Strategist and Karim El-Ghazaly, Equity Strategist.

]]>24 January 2026

Amr Hussein Elalfy

Almost 30 years ago, I had a discount brokerage account in the United States, through which I traded US stocks. One day, I received a communication message from my broker giving me the option to choose between several money-market funds that they offered. Two facts stood out to me at the time:

- The promised net asset value per fund share of these funds was USD1 at the end of every day as interest is usually distributed as more fund shares.

- The fund share may lose value because it is cash-like but not exactly cash because it is always marked to market on a daily basis.

In the United States, money-market funds usually invest in US Treasury bills, government agency securities, commercial paper, and bank certificates of deposit (CDs)—with an average maturity usually under 60 days. However, in Egypt, money-market funds are different, and so are fixed-income funds.

Here is what you need to know before investing your hard earned money in either money-market or fixed-income funds.

Fixed income for diversification

In our Egypt – 2026 Fundamental Strategy Series, we highlighted that it is important for investors to diversify their portfolios between three main asset classes:

- Equity

- Fixed income, and

- Gold.

In doing so, we recommended three strategic asset allocations (SAA) for each asset class depending on each investor’s risk profile, whether conservative, average, or aggressive. The more conservative investors are, the more weight they should have in the fixed income asset class. For the recommended weights for each risk profile, please read our Egypt – 2026 Fundamental Strategy Series.

In Egypt, fixed income instruments can range from banks’ CDs and time deposits to Treasuries, which investors can buy from banks. The only trick here is that it is not as easy to exit without losing some interest. This is where money-market and fixed-income funds come into play.

But let’s first define what money-market and fixed-income funds are.

What are money-market and fixed-income funds?

Money-Market Funds

These are designed to help investors park their cash while earning a return. They invest in short-term instruments, such as Treasury bills and bank deposits, with maturities of less than one year. These funds offer high liquidity and relatively stable performance, making them suitable for short-term savings and cash management rather than long-term investing.

Fixed-Income Funds

These invest in longer-term debt instruments, including government bonds, floating-rate notes, corporate bonds, and sukuks. Because these instruments are sensitive to changes in interest rates, the value of fixed-income funds can rise or fall over time. These funds are suitable for investors seeking higher returns (vs. money-market funds) and willing to accept price fluctuations over a medium- to long-term horizon.

Choosing between money-market and fixed-income funds?

For investors to choose between money-market and fixed-income funds, it is best to compare them given their different attributes, which we summarize in the below table from an investor’s and a fund’s view:

| Attribute | Money-Market Fund | Fixed-Income Fund |

| An investor’s view | ||

| Investing purpose | Liquidity parking | Yield / macro positioning |

| Typical holding period | Days to months | 1 to 5+ years |

| Return | More stable, more predictable | Less stable, less predictable |

| NAV volatility | Very low | Low to moderate, can be material |

| Income main source | T-bill yield | Coupons + capital gains |

| A fund’s view | ||

| Duration (interest rate sensitivity) | Lower | Higher |

| Interest rate decisions by CBE | A more quickly impact | A delayed impact |

| Reaction to rate hikes | Less negative | More negative |

| Reaction to rate cuts | Less positive | More positive |

| Fund holdings & maturity |

|

|

| Revaluation frequency (more on fund revaluation below) | Daily (marked to market) |

|

Source: Rumble Research

What does “fund revaluation” mean?

In calculating the fund’s net asset value (NAV), fixed-income funds tend to reevaluate their holdings depending on the accounting treatment applied to the securities they hold.

For instance:

- Instruments classified as held to maturity (HTM) are carried at amortized cost and are therefore not impacted by daily market price movements

- Securities measured at fair value or marked to market (MTM) are revalued periodically and reflect changes in interest rates and market conditions.

For valuation purposes, liquid securities are typically priced using the average traded price of the day, while illiquid instruments are valued using the last available transaction price—all quoted on the Egyptian Exchange.

Although certain provisions, such as accrued expenses or tax-related items, are purely accounting entries and do not negatively affect NAV, they often have a slightly positive impact through income accrual.

Reevaluation, on the other hand, is triggered either by regulatory requirements, as IFRS mandates periodic fair-value assessment, or by practical considerations, such as increased redemption activity that necessitates greater liquidity and may force a reclassification from HTM to MTM.

Mark-to-market valuation is particularly favorable in a declining interest rate environment, as bond prices rise, and it also gives fund managers greater flexibility to actively trade and realize capital gains.

The bottom line

In a nutshell:

- Money-market funds are cash-management tools with minimal duration risk (interest rate risk), while

- Fixed-income funds are rate-sensitive investment vehicles whose returns depend heavily on the interest-rate cycle and bond price movements.

If you are an investor with a short-term investment horizon and looking to park some cash on the sideline, then money-market funds are for you.

On the other hand, if you are an investor with a long-term investment horizon and looking to generate higher returns over time, then fixed-income funds are for you but you need to keep in mind that fixed-income funds are more volatile when it comes to the impact of revaluation which is usually positive when interest rates decline and negative when interest rates increase.

In view of the current easing cycle by the Central Bank of Egypt (CBE), long-dated debt securities should benefit the most. Thus, fixed-income funds will be more positively impacted by lower interest rates as opposed to money-market funds.

On Thndr, there are currently a total of 10 fixed-income funds that can be split between money-market funds and fixed-income funds, which you can choose from to match your profile:

| Money-Market Funds (Asset Manager) | Fixed-Income Funds (Asset Manager) |

| 1. ADM – Diamond Fund (AAIM) | 1. ABR – Bareeq (AAIM) |

| 2. ATD – Al Ahly Tamayoz Dividends (AFIM) | 2. BSC – B Secure (Beltone) |

| 3. AZN – AZ Nasser Fund (Azimut) * | 3. AIS – Istithmar wi Aman (AAIM) |

| 4. AZS – AZ Savings Fund (Azimut) | |

| 5. MTF – Misr Takaful Fund (AAIM) * | |

| 6. PCM – PFI Cashi Fund (PFI) | |

| 7. PGM – GIG Money Market (PFI) |

* Sharia compliant

Source: Thndr

]]>Cairo, Egypt – December 2025

Thndr, Egypt’s leading digital investment platform, announced today that it has obtained Asset Management and Portfolio Management licenses from the Financial Regulatory Authority (FRA). This milestone marks a significant expansion of Thndr’s ability to design and manage investment products built first and foremost for everyday individuals, rather than the institutional-first products that have traditionally dominated the market.

The licenses represent the next chapter in Thndr’s mission to make wealth-building simple, accessible, and affordable for all. Today, more than 431,000 Egyptians invest in mutual funds through Thndr, making it one of the country’s largest digital distributors of professionally managed investment products. With the new approvals, Thndr will begin creating its own suite of funds that are digital, transparent, low-cost, and tailored to real financial goals. The company plans to launch the first Thndr-managed funds in 2026.

Thndr’s movement into providing access to mutual funds four years ago was rooted in a clear insight: many people want to benefit from investing, but do not have the time or expertise to manage their portfolios day to day. Mutual funds effectively allow individuals to hand their money to a licensed, regulated expert who manages it alongside hundreds of millions – and sometimes billions – on their behalf. Since introducing access to these products, Thndr has seen exceptional growth that reflects a major shift in how Egyptians are choosing to save and invest. Mutual fund assets on the platform have reached EGP 8 billion as of November 19, 2025, up from EGP 575 million in January 2024 and EGP 1.2 billion in November 2024. Participation continues to grow across gold, fixed-income, and equity strategies, with gold funds such as AZG attracting more than 110,000 investors, while Thndr’s own fixed-income solution, Savings Clouds powered by a mutual fund, has scaled to EGP 2.46 billion. Over the past year, Thndr has also expanded its fund marketplace from 12 to 30 products, becoming one of Egypt’s most diversified platforms for everyday investors.

This momentum underscores a rising demand for simple, transparent, and professionally managed investment tools that align with real-life goals. By securing FRA asset management licenses, Thndr is now positioned to build the next generation of these products directly, and to do so with a retail-first lens that prioritizes accessibility, affordability, and ease of use.

Leading this strategic expansion is Dalia Shafik, appointed Head of Asset Management. With more than two decades of experience managing some of Egypt’s most successful funds, Shafik will oversee the development, governance, and operations of Thndr’s upcoming investment products.

“Mutual funds in Egypt have historically been built with institutions as the primary customer,” said Ahmad Hammouda, Co-founder and CEO of Thndr. “Over the past five years, we worked alongside existing asset managers to democratize access to these products digitally and give everyday people the same opportunities as institutions. Securing these licenses is the natural next step. It allows us to build funds designed for individuals from day one. Thndr is on a mission to offer the best investment experience at the lowest price to every person, and this milestone brings us one step closer to achieving that.”

“Thndr has already proven that retail investors want simple and powerful tools,” added Shafik. “Our next chapter is about designing those tools ourselves and ensuring they reflect people’s actual needs and goals.”

Thndr’s expansion into asset management builds on several years of market leadership. In 2024, the company executed 15.6 million trades worth EGP 174 billion, captured 11 percent of Egypt’s retail market share, and onboarded 82 percent of all newly coded retail investors into the Egyptian Exchange (EGX). With more than 4 million registered users, Thndr remains the country’s most inclusive digital gateway to investing.

About Thndr

Thndr is one of MENA’s first fully digital investment platforms, simplifying and democratizing investing for over 4 million users. The platform empowers investors through access to Egyptian stocks, gold, mutual funds, and savings products. Founded in 2020 by Ahmad Hammouda and Seif Amr, Thndr secured the first brokerage license issued in Egypt since 2008 and currently holds regulatory licenses from both the FRA (Egypt) and ADGM (UAE). To date, Thndr has raised a total of $37.76 million from global venture capital firms including Tiger Global, Prosus Ventures, BECO Capital, and Y Combinator. For more information, visit https://Thndr.app.

]]>26 November 2025

Amr Hussein Elalfy

In this note, we lay down an arbitrage strategy that shareholders in Macro Group [MCRO] can use to their benefit. MCRO is undergoing an EGP570mn capital increase with the following details:

- Rights trading: From 18 through 30 November 2025, after which they will expire.

- Subscription to the capital increase: From 18 November through 3 December 2025 for those who are rights holders.

Here is a link to the arbitrage strategy to apply at market price.

In sum, for existing MCRO shareholders, here are the decision rules:

| If the price of MCRO’s | is | The price of MCRO’s | then | Current status |

| right + 0.20 | lower than | stock | Buy the right then subscribe | Active |

| right + 0.20 | higher than | stock | Sell the right and buy the stock | Inactive |

Note: Arbitrage should be one right per one share.

Source: Rumble Research

How MCRO’s shareholders can benefit

What happened?

MCRO is currently undergoing an EGP570mn capital increase by issuing 2.85bn shares at a par value of EGP0.20 a share with no issuance fees. Thus, MCRO will be raising its paid-in capital from a current EGP114mn (570mn shares at a par value of EGP0.20/share) to EGP684mn (3.42bn shares at a par value of EGP0.20/share).

MCRO’s capital increase

| MCRO | No. of shares | Par value (EGP) | Paid-in capital (EGP) |

| Current | 570,206,456 | 0.20 | 114,041,291 |

| Subscription | 2,851,032,280 | 0.20 | 570,206,456 |

| New | 3,421,238,736 | 0.20 | 684,247,747 |

Source: Company reports, Rumble Research

The arbitrage strategy

In view of the current market prices, we are proposing an arbitrage strategy that is directed at existing MCRO shareholders given that MCRO’s right is currently trading at a deep discount to MCRO’s stock.

Who is it for?

This strategy is only applicable to existing MCRO shareholders who:

- Currently own MCRO shares.

- Intend to hold on to their MCRO shares for at least the next 2-3 months.

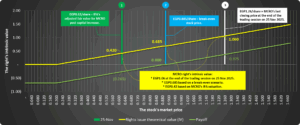

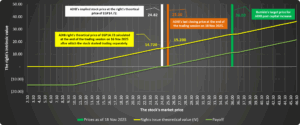

MCRO’s tradable rights intrinsic value vs. payoff

Source: Rumble Research

Key price levels to keep in mind

| No. | MCRO (stock price) | MCROr (right price) | MCROr (intrinsic value) | MCROr (payoff) | Comment |

| 1 | 0.620 | 0.685 | 0.420 | (0.265) | EGP0.620/share is the price at which the right produces a negative payoff. |

| 2 | 0.885 | 0.685 | 0.685 | 0.000 | EGP0.885/share is the price at which the right produces a zero payoff (break-even). |

| 3 | 1.260 | 0.685 | 1.040 | 0.375 | EGP1.260/share is yesterday’s market price at which the right produces a positive payoff (i.e. the right is cheaper than the stock). |

Source: Rumble Research

What are the risks?

Currently, the right is trading at a discount to the stock, so in essence existing MCRO shareholders who are in the stock for the long term can make some money by selling their stock (sell high) then use that money to buy the right (buy low).

However, to benefit from this, they need to buy the right at the same time they are selling the stock, so that market fluctuation does not impact the final payoff.

The key risk is that MCRO’s stock price is currently trading at a huge premium (more than double) to the independent financial advisor’s (IFA) fair value post-capital increase of EGP0.62/share. Thus, those opting to hold on to MCRO shares after the rights are exercised face the market risk that MCRO stock price may fall in the future.

It is their decision then to either:

- Sell the stock once the subscription shares are made available in 2-3 months’ time, provided they are profitable.

- Continue to be long-term shareholders in the stock.

Investment Disclaimer

This document is for informational purposes only and should not be construed as a solicitation, offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or to provide any investment advice or service.

The information used to produce this market commentary is based on sources that Rumble Research (“Rumble”) believes to be reliable and accurate. This information has not been independently verified and may be condensed or incomplete. Rumble does not make any guarantee, representation, or warranty and accepts no responsibility or liability as to the accuracy and completeness of such information. Expression of opinion contained herein is based on certain assumptions and the use of specific financial techniques that reflect the personal opinions of the authors of the commentary and is subject to change without notice. It is acknowledged that different assumptions can always be made and that the particular technique(s) adopted, selected from a wide range of choices, can lead to a different conclusion. Therefore, all that is stated herein is of an indicative and informative nature, as forward-looking statements, projections, and fair values quoted may not be realized. Accordingly, Rumble does not take any responsibility for decisions made on the basis of the content of this commentary.

The decision to subscribe to or purchase securities in any offering should not be based on this report and must be based only on public information on such security.

Recommendations and general guidance are not personal recommendations for any particular investor or client and do not take into account the financial, investment, or other objectives or needs of, and may not be suitable for, any particular investor or client. Investors and clients should consider this only a single factor in making their investment decision, while taking into account the current market environment.

Neither Rumble nor any officer or employee of Rumble accepts liability for any direct, indirect, or consequential damages or losses arising from any use of this report or its contents.

Intellectual Property Rights: No part of this document may be reproduced without the written permission of Rumble. The information within this research report must not be disclosed to any other person if and until Rumble has made the information publicly available.

]]>Here is what you need to know about Abu Dhabi Islamic Bank – Egypt’s capital increase and what to do with its tradable rights.

19 November 2025

Amr Hussein Elalfy

In this note, we lay down the story behind Abu Dhabi Islamic Bank – Egypt’s [ADIB] EGP3bn capital increase and the different options available to you as an existing shareholder or as a prospective shareholder, whether you should sell your rights or exercise them. And here you are some dates to keep in mind:

- Rights trading: From 19 November through 1 December 2025, after which they will expire. Thus, you need to make up your mind during that period.

- Subscription to the capital increase: From 19 November through 4 December 2025 for those who are rights holders.

But let’s first remember what the stock exchange is important for.

A marketplace for everyone

The stock exchange is often looked at as an “exit market” when existing shareholders of companies sell their shares to new shareholders (investors) often at a premium to their original cost of acquisition. However, the stock exchange is not only a marketplace where sellers can dispose of their shares. In fact, the most important role of a stock exchange is for companies to raise required capital from existing shareholders or investors at large to support their growth.

Thus, the stock exchange is indeed a marketplace for everyone: a marketplace for “existing” shareholders to raise liquidity by selling their “existing” shares and a marketplace for companies to raise capital by selling “new” shares to “new” investors.

Two examples

Let’s take two quick examples.

If a privately-held company wants to raise capital, it can do so through an initial public offering (IPO) by issuing new shares to investors (potential new shareholders). This is known as a primary offering, similar to what Bonyan for Development & Trade [BONY] did in its IPO when it raised EGP250mn as part of the IPO process.

On the other hand, if a listed company wants to raise capital, it can do so by calling on its existing shareholders to shore up new capital to fund their operations and/or reduce debt, for example. This is what Abu Dhabi Islamic Bank Egypt [ADIB] is doing today.

What about ADIB’s tradable rights?

What happened?

ADIB is currently undergoing an EGP3bn capital increase by issuing 300mn shares at a par value of EGP10 a share in addition to EGP0.10 a share as issuance fees. All in all, the bank will potentially raise a total of EGP3.03bn at the end of the day if the capital increase is fully covered. Thus, ADIB will be raising its paid-in capital from a current EGP12bn (1.2bn shares at a par value of EGP10/share) to EGP15bn (1.5bn shares at a par value of EGP10/share).

Know your options: Who gets what?

Each group of investors (existing or new ADIB shareholders) will have several options to consider.

Existing shareholders

This capital increase was available for ADIB’s existing shareholders at the end of 16 November 2025 at a ratio of 1-to-4 (300mn “new” shares for 1.2bn “existing” shares). This means if you were a shareholder as of that date and say you owned 100 shares, today you would have the same 100 shares plus 25 rights that you can use to subscribe to 25 new shares.

Available options

These existing shareholders have two options:

- Exercise the right to subscribe to the capital increase, especially if you think ADIB’s stock is undervalued and you believe in the long-term value of the bank’s franchise.

- Sell the right for any particular reason, such as:

- You do not have enough cash to shore up for the capital increase.

- You want to raise liquidity by partially exiting your investment in ADIB.

- You think ADIB’s stock is overvalued.

Investors (new shareholders)

An ADIB existing shareholder who decides to forgo the opportunity to participate in the bank’s capital increase can sell the rights in the market, where either other existing ADIB shareholders or investors who are non-shareholders would buy them.

Available options

These investors have two options:

- Exercise the right to subscribe to the capital increase, assuming they think ADIB’s stock is undervalued and they believe in the long-term value of the bank’s franchise.

- Sell the right if its market price rises beyond their acquisition cost so that they can generate a positive return.

All options in charts

To make things even more crystal clear, we need to consider the rights as a call option that grows in value as the underlying stock (ADIB in this case) grows in value.

Source: Rumble Research

Key price levels to keep in mind

| EGP/share (EGP/right) | ADIB (stock) | ADIBr (right) | Subscription price |

| ADIB’s stock price adjusted for the rights (16 Nov 2025) | 24.82 | 14.72 | 10.10 |

| ADIB’s stock price (18 Nov 2025) | 25.30 | 15.20 | 10.10 |

| ADIB’s target price (Rumble) | 36.00 | 25.90 | 10.10 |

Source: Rumble Research

Now what?

Given that ADIB is an open fundamental recommendation that we have, we believe the stock is undervalued. Our latest target price based on a 1.2bn share count was EGP42.5 a share. This is a pre-capital increase valuation. Assuming the capital increase is fully covered, which we think it will be, then the post-capital increase target price is now EGP36 a share, implying a 42% upside from the latest closing price of EGP25.30 a share.

Recommended actions

We maintain our INVEST rating on ADIB, which also means we recommend for existing shareholders to subscribe to the capital increase. This is in view of its above-average growth rate and potential windfall from its upcoming capital increase. We believe the capital increase will help grow the bank’s balance sheet and eventually drive growth and profitability higher further.

Meanwhile, keep the following in mind:

| If the price of ADIB’s | is | The price of ADIB’s | then |

| For ADIB existing shareholders | |||

| right + 10.10 | lower than | stock | Buy the right then subscribe |

| right + 10.10 | higher than | stock | Sell the right and buy the stock |

| For other investors | |||

| right + 10.10 | lower than | stock | Buy the right then subscribe |

| right in the market | higher than | right (at acquisition) | Either sell the right at a profit or keep it to subscribe |

| right in the market | lower than | right (at acquisition) | Keep the right then subscribe |

Note: In any case, if the market price of the right rises higher than the price at which you acquired it, you can sell it in the market at a profit.

Source: Rumble Research

Investment Disclaimer

This document is for informational purposes only and should not be construed as a solicitation, offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or to provide any investment advice or service.

The information used to produce this market commentary is based on sources that Rumble Research (“Rumble”) believes to be reliable and accurate. This information has not been independently verified and may be condensed or incomplete. Rumble does not make any guarantee, representation, or warranty and accepts no responsibility or liability as to the accuracy and completeness of such information. Expression of opinion contained herein is based on certain assumptions and the use of specific financial techniques that reflect the personal opinions of the authors of the commentary and is subject to change without notice. It is acknowledged that different assumptions can always be made and that the particular technique(s) adopted, selected from a wide range of choices, can lead to a different conclusion. Therefore, all that is stated herein is of an indicative and informative nature, as forward-looking statements, projections, and fair values quoted may not be realized. Accordingly, Rumble does not take any responsibility for decisions made on the basis of the content of this commentary.

The decision to subscribe to or purchase securities in any offering should not be based on this report and must be based only on public information on such security.

Recommendations and general guidance are not personal recommendations for any particular investor or client and do not take into account the financial, investment, or other objectives or needs of, and may not be suitable for, any particular investor or client. Investors and clients should consider this only a single factor in making their investment decision, while taking into account the current market environment.

Neither Rumble nor any officer or employee of Rumble accepts liability for any direct, indirect, or consequential damages or losses arising from any use of this report or its contents.

Intellectual Property Rights: No part of this document may be reproduced without the written permission of Rumble. The information within this research report must not be disclosed to any other person if and until Rumble has made the information publicly available.

]]>This is all you need to know about TWSA’s IPO.

Amr Hussein Elalfy

30 October 2025

The Story

A nascent industry with room for exponential growth

Factoring in Egypt is a relatively nascent industry. It began only 18 years ago when Egypt Factors, initially backed by Commercial International Bank [COMI], became the first licensed factoring company in the country and remained so for the following 4.5 years. Today, there are 37 factoring companies licensed in Egypt with a total portfolio size of EGP43.7bn at the end of 30 June 2025, only 0.3% of Egypt’s GDP. This compares to around 5% of GDP in emerging markets. This potentially implies that Egypt’s factoring industry has room to grow 15x its current size.

TWSA helps SMEs manage their working capital needs …

In July 2020, Tawasoa Factoring [TWSA] acquired its license, led by a group of entrepreneurs whose goal was to create Egypt’s first non-banking financial institution fully dedicated to factoring. Capitalizing on the expertise and diverse professional backgrounds of its founders, TWSA’s aim is to bridge the gap in the Egyptian market, helping small- and medium-sized businesses unlock the power of their receivables. TWSA offers premium, fast, and tailor-made factoring solutions, thus supporting its clients in managing their working capital needs to ensure continued growth, enhance cash flows, and drive expansion.

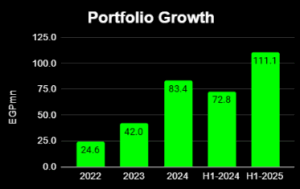

… with portfolio size set to double by 2026 …

With a portfolio size of EGP111mn at the end of 30 June 2025, TWSA’s market share stood at only 0.3% of the factoring industry in Egypt. The company’s plan is to more than double its portfolio to EGP260mn by the end of 2026.

… hence, the need to grow its capital

TWSA’s paid-in capital has been on the rise since its establishment. It grew 5 fold from EGP15mn at the end of 2021 to EGP75mn currently. To further drive its next chapter of growth, TWSA has made the strategic decision to list on the SME Exchange (previously known as Nilex). It plans to later call for an EGP40mn capital increase to grow its equity capital 1.5x to EGP115mn within the next couple of months.

The IPO

- TWSA will go public on the SME Exchange through a public and private offering with the following details:

| Number of shares offered in the IPO | 18,750,000 |

| Estimated stake | 25% |

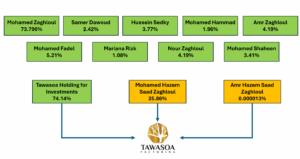

| Selling shareholder | Mohamed Hazem Saad Zaghloul Mohamed

|

| IPO price | EGP1.73 a share |

| Estimated IPO size | EGP32.4mn |

| Subscription period | Sunday, 2 Nov – Thursday 6 Nov 2025 |

| Private tranche

(Qualified investors only) |

|

| Public tranche |

|

| Stock price stabilization fund |

|

Source: EGX, Company prospectus.

The Capital Increase

- According to TWSA’s prospectus, within 60 days following the end of the stock price stabilization fund, TWSA plans to undergo a capital increase of EGP40mn (40mn new shares at a par value of EGP1/share).

- All existing shareholders (including those who subscribed in the IPO) will be eligible to subscribe to the capital increase.

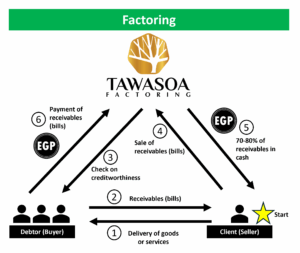

What is Factoring?

Factoring is a financial service that helps businesses turn their invoices into immediate cash. Instead of waiting for customers to pay, a business can sell its accounts receivable to a third party, called a factor, at a discount. This gives the business quick access to funds, helping it manage its expenses and maintain steady cash flows. Factoring is especially useful for SMEs that face long payment cycles or need quick financing to support their operations and growth.

How Factoring Works

Factoring transforms unpaid invoices into a source of immediate liquidity, turning waiting time into working capital as follows:

- The Client (Seller) starts by selling its unpaid invoices to the factor.

- In return, the Factor instantly provides around 70–80% of the invoice value, giving the business access to cash within days instead of months.

- When the Debtor (Buyer) settles the invoice, the factor releases the remaining balance to the business after deducting a small fee, thus netting a profit.

This process allows companies to focus on growth and operations rather than chasing payments or facing cash shortages. In essence, factoring converts potential into power, enabling businesses to move forward without financial delays.

Parties Involved

- Client (Seller): The business that sells its invoices to receive instant cash.

- Factor (Tawasoa Factoring): The financial institution that purchases the receivables and provides the funding.

- Debtor (Buyer): The customer that owes payment on the invoice.

Source: Rumble Research

Key Advantages

- Immediate cash flow: Converts unpaid invoices/bills into instant funding to cover expenses or support growth.

- No debt incurred: Provides financing through the sale of receivables rather than borrowing.

- Flexible and scalable: Funding grows in line with sales and receivables.

- Simplified collections: The factor manages customer payments, saving time and effort.

- Risk reduction: Factors assess customer creditworthiness, lowering exposure to bad debts.

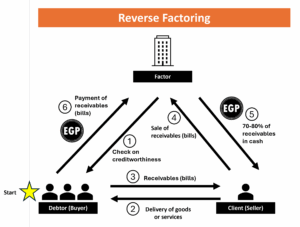

What is Reverse Factoring?

Note: TWSA does not currently offer reverse factoring, but it plans to do so in the future.

Reverse factoring, also known as supply chain financing, is a financial solution designed to support both buyers and their suppliers. Unlike traditional factoring, where the supplier (seller) initiates the transaction, reverse factoring is typically arranged by the debtor (buyer) to help suppliers receive early payment on their invoices.

In this arrangement, a financial institution (the factor) pays the supplier (seller) on behalf of the debtor (buyer) before the invoice’s due date. The buyer then repays the factor at a later, agreed-upon date. This process improves the supplier’s cash flow while allowing the buyer to maintain longer payment terms — creating a mutually-beneficial relationship across the supply chain.

How Reverse Factoring Works

- The supplier delivers goods or services and issues an invoice to the buyer.

- The buyer confirms the invoice and approves it for payment.

- The factor pays the supplier early, typically covering 100% of the invoice amount minus a small fee.

- On the agreed due date, the buyer repays the factor in full.

This process creates a win–win dynamic: suppliers receive immediate liquidity and reduce financial pressure, while buyers strengthen their supply chains and may even negotiate better terms with suppliers.

Parties Involved

- Debtor (Buyer): The company purchasing goods or services and initiating the financing arrangement.

- Client (Seller): The company providing goods or services and receiving early payment.

- Factor (Financial Institution): The intermediary that pays the supplier and later collects payment from the buyer.

Source: Rumble Research

Key Advantages

- For Sellers (Suppliers): Provides faster access to cash and lowers the risk of delayed payments.

- For Buyers: Helps maintain stronger supplier relationships and ensures stability in the supply chain.

- For Both: Enhances operational efficiency and reduces financing costs through collaboration.

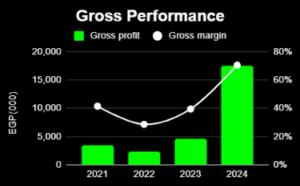

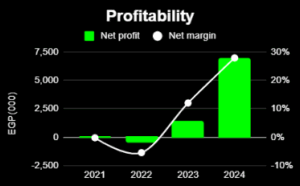

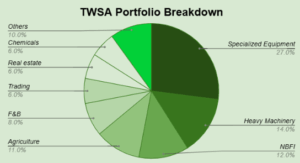

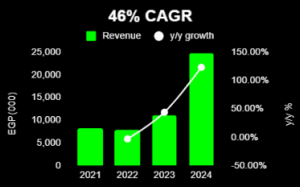

TWSA in Charts

Source: Company reports.

IFA Valuation

TWSA’s fair value was set by the independent financial advisor (IFA) at EGP1.73 a share, valuing the company at around EGP130mn (based on a 75mn share count). To reach its fair value, the IFA used two valuation methods:

- Residual income model (70% weight): The model basically considers the residual income generated by the company (i.e. the economic profit in excess of the company’s equity capital charge), projects a terminal growth rate, then discounts all to the present value to add to the company’s existing book value of equity. This approach yielded a fair value of around EGP135mn or EGP1.80/share, net of a 5% discount for the lack of control given the relatively small size of the stake offered.

- Price-to-book multiple (30% weight): This method looked at a list of comparable companies trading on the EGX within the financial sector (which included listed banks), reaching an average P/BV of 1.45x. This approach yielded a fair value of around EGP117mn or EGP1.56/share.

The Bottom Line

When it comes to investing in a non-banking financial services (NBFS) firm, what really matters is its profitability relative to its capital base. As for TWSA, it is going in the right direction, growing its portfolio and profitability. However, TWSA needs to reach its critical mass in terms of equity capital to unlock its growth potential, which it hopes to do with its proposed capital increase following its listing. On one hand, being a small-cap stock trading on the SME Exchange may limit the number of investors who will be willing to take on the risk of a company of this size. On the other hand, if TWSA manages to grow its capital base then graduate to the main market, this could be a catalyst for its stock performance.

For a more detailed view on TWSA’s valuation and what to do with the stock, you can subscribe to Rumble.